A possible second East and Gulf Coast port strike in January and concerns over anticipated tariffs levied by the incoming Trump administration won’t slow down American consumer demand in 2025, according to a top bellwether of global trade.

Container shipping giant Maersk expects global trade growth of up to 7 percent next year, one of its top execs told Reuters Wednesday at the news agency’s Next conference.

“We predict anywhere between 5 percent and 7 percent (growth) overall,” Charles van der Steene, regional president for North America at Maersk, said. “And at this stage, there’s nothing that would indicate that it could not be the case.”

Related Stories

Even the bear end of the projection would be a strong increase over 2024. According to a December update from UN Trade and Development (UNCTAD), global trade is expected to grow 3.3 percent this year to $33 trillion.

It would also be a more optimistic projection than the World Trade Organization (WTO), which said in October that trade volume growth for 2024 should come in at around 2.7 percent while growth in 2025 is expected to reach 3 percent.

The ocean carrier already upwardly revised a metric that mirrors that of a global trade—global container market volume growth—for the full year, saying it would expand 6 percent in 2025. Previously, Maersk called for growth between 4 percent and 6 percent, illustrating the shift in container market demand through the year and the even heavier shift in sentiment. As recently as August, Maersk CEO Vincent Clerc called container demand the biggest question mark of the 2024 second half.

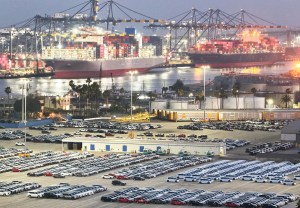

North American consumers are making up a heavy chunk of the demand spurring the growth. In the first three quarters, North American market imports for Maersk grew between 20 percent and 24 percent across the first three quarters, with van der Steene telling CNBC on Friday that the company expects fourth-quarter growth numbers to remain in the double digits.

Imports continue to enter the U.S. in droves largely due to the concerns regarding the potential January port strike and Trump’s inauguration. Major ports handled 2.25 million 20-foot equivalent units (TEUs) in October, a 9.2 percent increase over the year prior and a record for the month, according to the Global Port Tracker shared by the National Retail Federation.

November and December numbers are both expected to crack the 2.1 million TEU mark, before bumping up further to 2.2 million containers in January—yet another indicator that U.S.-driven demand seems to be pulling up worldwide trade growth.

If anything, the catalysts of the cargo front-loading are showcasing that global trade will likely continue to endure in a high-disruption environment, with van der Steene telling CNBC that more shipping companies expect the volatility to continue through next year. “Disruption will also be with us,” he said. “The topic of resilience within the supply chain will continue to be, and should be, on everyone’s agenda.”

This volatility and disruption has been a constant since the peak of Covid-19, but the onslaught of attacks in the Red Sea by Yemen-based Houthi militants since November 2023 has further ensured that the container shipping industry will have to endure longer lead times.

Additionally, ocean carriers like Maersk now must adjust to the “new normal” of Asia-to-Europe trade around Africa’s Cape of Good Hope, rather than the Suez Canal. Even optimistic projections like those from Maersk don’t expect a return to the waterway until well into 2025.

As situations like the Red Sea crisis add 10-to-14 days to many deliveries and contribute to worldwide port congestion—all while trade volumes are expected to further increase—some have suggested that overcapacity within the industry remains a concern.

One of the wider responses to the anticipated increase in container demand has been the continued surge of new vessel deliveries. Roughly 3.15 million TEUs of new shipping capacity is expected this year, following the 3.16 million TEUs delivered in 2023, according to S&P Global Market Intelligence.

Maersk’s Clerc seemed to downplay the impacts from overcapacity going into 2025.

“Our capacity has increased, but this extra capacity has been absorbed in longer sailing distances,” said Clerc in an Oct. 31 earnings call. “We simply did not have the amount of slack capacity that maybe some of our competitors had to cater for that unexpected strong demand on top of long sailing routes.”