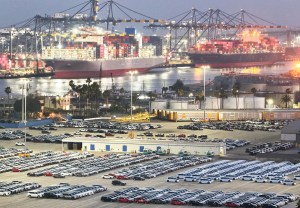

After nearly 14 months of attacks by Houthi militants, the Red Sea appears no closer to being free of disruption than it did when top ocean carriers elected to avoid the waterway on their journeys.

Although the Red Sea crisis has brought chaos to the shipping industry and global supply chains at large in the form of lengthier delivery times, more port congestion and an increase in carbon emissions, the diversions may have inadvertently helped alleviate another potential problem—overcapacity.

Related Stories

According to data from container shipping research tool and database Alphaliner, the global container fleet increased by 10.6 percent during the past 12 months, with almost 3 million 20-foot equivalent (TEUs) of slots added to the fleet.

Fifty-nine percent, or 1.76 million TEUs, of this extra capacity was absorbed by the Asia-to-Europe trade, where many additional ships were needed as diversions around southern Africa’s Cape of Good Hope persisted.

Over the past year, fleet growth dedicated to that trade lane has increased 31 percent, with some carriers still awaiting the delivery of more newbuildings to fill the final gaps in their Asia-to-Europe schedules.

However, average weekly TEU capacity offered on the Asia-to-Europe route has risen by a much smaller percentage—8.8 percent—as the longer routes kept soaking up space on the vessels, indicating that the new slots had been filling up quickly.

“The year 2024 will be remembered in liner shipping circles as the (first) year of the Red Sea crisis, just as 2021 and 2022 are now commonly referred to as the lucrative Covid-19 years,” Alphaliner said in a post on LinkedIn. “While many commentators were warning of potential overcapacity in 2024, finally the Cape diversions absorbed so much capacity that the industry terminated the year with almost no idle tonnage (just 0.6 percent of the total container ship fleet was deemed commercially inactive).”

Overcapacity had been a concern at the start of 2024 due to container shipping firm’s hefty order book of vessels in the years after global supply chain congestion at sea reached then-unprecedented levels.

But fast forward to today, and even Maersk’s CEO has downplayed the idea that there would be too many ships at sea in 2025.

“Our capacity has increased, but this extra capacity has been absorbed in longer sailing distances,” said Maersk’s Vincent Clerc in an Oct. 31 earnings call. “We simply did not have the amount of slack capacity that maybe some of our competitors had to cater for that unexpected strong demand on top of long sailing routes.”

That’s not to say that there still isn’t caution in the industry. In a Nov. 20 earnings call, ZIM chief financial officer Xavier Destriau said “the risk of oversupply continues to exist,” given the company’s recent growth in order book-to-fleet ratio to 25.5 percent.

Another factor in shipping’s favor is “it’s not an if, it’s a matter of when” older ships will be scrapped or retired, Destriau said. He also noted that ships in 2024 are sailing at 16.5 knots on average to handle the longer routes, up from 15.5 knots in 2023. The faster speed is an indicator that ships would be able to cope with a surge of required capacity, if necessary.

“That one knot difference is having a significant effect on capacity absorption,” said Destriau. “So when the route around via the Suez reopens, all those drivers will come in also to potentially mitigate the risk or the effect of this influx of capacity.”

Asia-to-Europe rates stabilize amid U.S. concerns

While container freight rates for cargo entering the U.S. have escalated over the past month as importers have front-loaded more goods ahead of a possible East and Gulf Coast port strike and potential tariffs by the incoming Trump administration, the same cannot be said for rates on the Asia-to-Europe trade lane even as the Red Sea crisis endures.

In fact, the rates have largely held steady since early December.

As of Thursday, container prices on the Shanghai-to-Genoa route were flat to the week prior, according to the Drewry World Container Index (WCI), at $5,420 per 40-foot container. Compared to four weeks ago, these containers are down 1 percent from $5,496 on average. The Shanghai-to-Rotterdam trade lane saw a slight weekly decline of 1 percent to $4,774 on average, and is flat from Dec. 5’s $4,775 per container.

In the event that the Red Sea crisis were to end, freight rates would likely plummet as ships returned to their normal routes, according to Flexport CEO Ryan Petersen, who told Bloomberg Surveillance Monday that it would “instantly bring the price of ocean freight down by two-thirds, maybe more.”