Although a possible second strike at the East and Gulf Coast ports was more than likely averted when union dockworkers and their employers signed a new tentative labor agreement Wednesday, U.S. importers hedged against its impacts by staying in front of it throughout the holiday season.

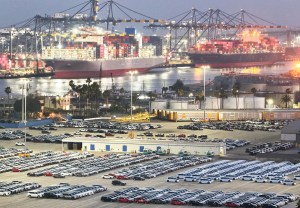

According to the Global Port Tracker report released by the National Retail Federation (NRF) and maritime trade consultancy Hackett Associates, the top U.S. ports handled 2.17 million 20-foot equivalent units (TEUs) in November, a 14.7 percent increase over the year prior. The data also marked a 3.2 percent decline from October, a much lighter drop than the 8.3 percent dip experienced month to month in 2023.

Related Stories

December is anticipated to see an even bigger annual increase, with the Global Port Tracker projecting the month at 2.24 million TEUs, up 19.2 percent year over year. That would bring 2024 to 25.6 million TEUs, up 15.2 percent from 2023.

2024’s expected inbound cargo volume would slightly surpass the 25.5 million containers reeled in during the 2022 calendar year, but remain 0.8 percent below the 25.8 million-TEU record set in 2021.

The forecasts for U.S. imports were much tamer ahead of the three-day International Longshoremen’s Association (ILA) strike on Oct. 1, and the November election of President-elect Donald Trump. At the time, November had been forecast at 1.91 million TEU and December at 1.88 million TEU, while the total for 2024 was forecast at 24.9 million TEU.

January is forecast at 2.16 million TEUs, up 10 percent year over year, as brands rushed product in ahead of a potential redux of an ILA strike. This number is slightly tapered from last month’s expectations for January of 2.2 million TEUs, signaling a minor softening due to the new ILA contract.

“The new contract brings certainty and avoids disruptions, and we hope to see it ratified as soon as possible,” said Jonathan Gold, vice president for supply chain and customs policy at the NRF, in a statement. “But the agreement came at the last minute, and retailers were already bringing in spring merchandise early to ensure that they would be well-stocked to serve their customers in case of another disruption, resulting in higher imports.”

Gold also pointed to President-elect’s Trump return to the oval office, and his plans to increase tariffs on countries including China, Mexico and Canada.

“Retailers want to avoid higher costs that will eventually be paid by consumers,” said Gold. “The long-term impact on imports remains to be seen.”

The Global Port Tracker also shared forecasts beyond January, when the uncertainties of the East and Gulf Coast labor situation are out of the picture and there’s a clearer understanding of what a second Trump administration’s trade policy will look like.

February’s inbound cargo volume is expected to be 1.87 million TEUs, down 4.5 percent because of Lunar New Year factory shutdowns in China. March should see a 10.6 percent bump in containers to 2.13 million TEUs. The next two months are supposed to see lighter, but still healthy, increases. April is projected to come in at 2.18 million TEUs, up 8 percent, while May should see a 5.9 percent increase to 2.2 million TEUs.

The flood of imports throughout 2024 and into the new year heavily impacted China, as factories have rushed to fill orders ahead of the Trump tariffs. While exports rose 5.9 percent to 25.5 trillion yuan ($3.6 trillion) last year, they increased as much as 10.7 percent in December, according to China’s General Administration of Customs.

For the time being, the cargo flurry has also impacted rates into the U.S. at a substantially stronger pace than for container volumes being transported back to Asia, or to major ports in Europe.

While the Jan. 9 Drewry World Container Index (WCI) increased just 2 percent week over week to $3,986 per 40-foot equivalent unit, the voyages from China into both Los Angeles and New York are propping the wider index up. The Shanghai-to-L.A. route saw a 13 percent bump to $5,476 per container, while the Shanghai-to-N.Y. trade lane experienced a 10 percent average price increase to $7,085 per unit.

When the data was released last Thursday, Drewry said it expected rates on the trans-Pacific trade to rise in the coming week, driven by the front-loading ahead of the anticipated tariff hikes.

Trump has previously said he will enact various tariffs on China, Mexico and Canada on the first day of his second presidency, which is set to begin on Jan. 20.