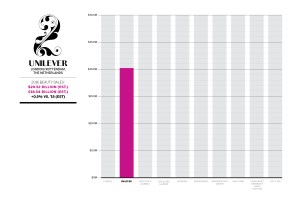

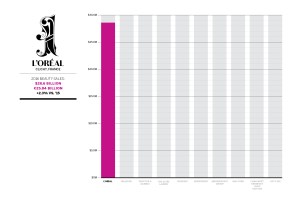

L’Oréal

L’Oréal benefitted from the global growth in the makeup segment and continued to move forward with its digital strategy in 2016. Within the Consumer Products division, makeup saw double-digit growth driven by NYX, Maybelline, L’Oréal Paris and Essie. The L’Oréal Luxe division grew 6% and e-commerce sales rose 33%. The strong growth at L’Oréal Luxe was boosted by the acquisition of two brands, niche fragrance label Atelier Cologne in July and fast-growing U.S. makeup brand It Cosmetics in August, which it bought for $1.2 billion.